http://www.zerohedge.com/sites/defau...for%20Sale.jpg

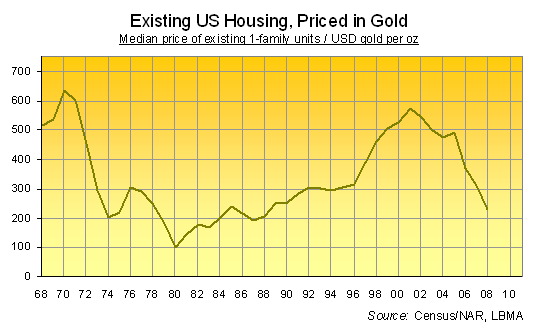

I'm NOT saying that housing won't go lower (it probably will)....

But American real estate is going to hit a bottom relatively soon. Solid down payment, fixed rate, a house you can AFFORD.

I think the end is near for the housing crash.

Commercial real estate? The blood bath is right around the corner....

Reply With Quote

Reply With Quote

Site Information

About Us

- RonPaulForums.com is an independent grassroots outfit not officially connected to Ron Paul but dedicated to his mission. For more information see our Mission Statement.

Connect With Us