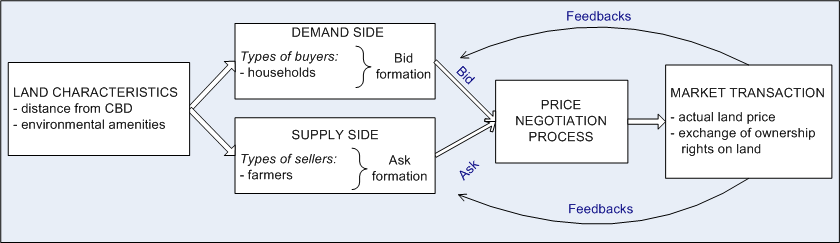

Here's a chart, a simplified version of a more general figure representing a comprehensive ABM market model described elsewhere (

Filatova, Parker et al. 2007;

Filatova , van der Veen et al. 2007;

Parker and Filatova 2008)) that illustrates this, including the supply/price relationship in economics:

Note how the actual market price of land is differentiated from the Ask price in the Ask formation. The "actual land price" or "market price" is to the right of SUPPLY SIDE. This is determined by actual transactions (i.e., when Bid=Ask ---> MARKET TRANSACTION). This market price (established, and always in the past) is no longer part of the supply, but only serves as informational feedback that helps both sellers and buyers in their future "Ask price formation" and "Bid price formation", respectively. But in a free market neither are bound by it, which is why market price (past) does not control supply or demand (present) which, when consummated as future transactions, determine future market price.

The

DEMAND SIDE and

SUPPLY SIDE (Bid/Ask formation) occur BEFORE market price is established, and as separate entities, which come together during the

PRICE NEGOTIATION PROCESS. Because the market price is determined by supply and demand, and not the other way around, there is lineage that leads back to an original transaction - for which a market price had yet to be established. Thus, no chicken/egg paradox exists for supply, because the FIRST SUPPLY of a thing does not require a market price. Only an Ask price.

The market price (as historical information) is often used by buyers and sellers in their respective Bid/Ask formation, but as decision making feedbacks only. It DOES NOT determine or control them, and is NOT, therefore, a controlling factor on supply or demand. Only buyers control the demand side (willingness to buy a specific quantity at a specific bid price), just as only sellers control the supply side (willingness to sell a specific quantity at a specific ask price).

Again, from that same source: (which shows the word "prices" in "ask" and "bid" context)

Supply is neither defined as nor controlled by what HAS BEEN made available for purchase in the past. It is constrained to the quantity that is NOW made available by sellers for FUTURE purchase at a given minimum

ask price.

Ask Price determines supply, not Market Price.

Thus, if a seller has 10 acres of land divided into ten 1 acre parcels, that seller can decide which of these parcels he is willing to make available to the market at a given price. The seller may even FIX that supply as a function of quantity (area) made available for a given price over a specified time (the seller's supply schedule). That's the supply of that land made available to the market, which has nothing to do with market price, the total quantity, or even whether any of it actually trades.

A little more reading for you, to help you understand: (emphasis mine)

I can see why it's important for you to remove the seller's decision making power and its role in supply as it relates to land, and why you would attempt to change well-established economics theory to make "market price" rather than "ask price" the determinant for supply. After all, if "supply" indeed equals the total quantity in existence, you can then claim that the supply itself fixed. But that is not reality, not the truth, and certainly not established economic theory as it relates to supply and demand.

You want to think of supply in terms of production only, such that anything rare, already in existence and non-reproducible as a factor of production as somehow ALL "available to the market" and therefore "fixed supply", on the basis that it exists in the aggregate in fixed quantity, which can then be placed somewhere on a supply curve. You erred in trying to a) make supply a function of the market price, not ask price, and b) assume that the seller's willingness to sell is only a matter of price, and c) ignore the fact that only a seller is in a position to create a supply curve in the first place! I tried accommodate your misapprehension in all of this by ignoring a and c, and saying that this could be true so long as you make the ask price range somewhere from ZERO to INFINITY. Then it could technically include all possibilities.

Infinity could be used to technically account for anything that that a seller is NOT willing to make available at any price (NO ASK EXISTS, NO BID WOULD BE ACCEPTED). You could plot that as INFINITY on the supply curve, because whatever a seller is NOT WILLING TO MAKE AVAILABLE AT ANY PRICE is, by definition, "priceless", and not available to the market, and therefore not normally counted as "supply". By referring to it as infinity, it's only a question of time, theoretically, before the possibility of that number coming down to some lower point on the supply curve. But that doesn't mean it's "available to the market", or that this could become the actual market price for that particular quantity, because it is impossible for anyone on the demand side to Bid infinity. But at least you could sneak it onto the supply curve.

You're talking "market price", and therefore history - not actual supply, as defined as the quantity now made available at a given ask price, for which a future market price has yet to be established.

Originally Posted by helmuth_hubener

Reply With Quote

Reply With Quote

Connect With Us